2024/3/15

In 2023, China’s clothing industry is facing a more complex and challenging external environment. Global economic growth has slowed down, and there is a contraction in international market demand, putting pressure on the clothing industry. Looking ahead to 2024, the situation for the apparel industry’s development remains complex and challenging. Apparel enterprises must continue to speed up innovation and development, build a modern industrial system, and drive the industry towards high-end, smart, sustainable, integrated development.

01 Production

According to the National Bureau of Statistics data, the industrial added value of apparel enterprises above the designated size declined by 7.6% year-on-year in 2023, 1.2 percentage points lower than the first three quarters. The garment production of enterprises above the designated size totaled 19.39 billion pieces, declining by 8.69% year-on-year, 0.7 percentage points narrower than the first three quarters of 2023.

02 Domestic sales

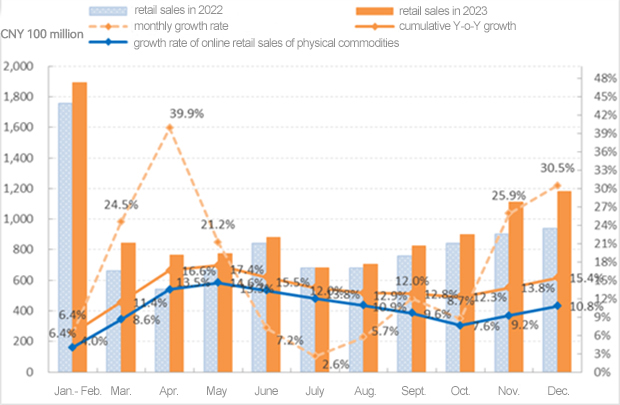

According to the National Bureau of Statistics, the total retail sales of consumer goods amounted to CNY 1.03 trillion, up by 15.4% year-on-year. In the fourth quarter, driven by the Singles Day shopping carnival, the seasonal sales of autumn and winter clothes, and the low base effect, the growth rate of retail sales of apparel above designated size reached 25.9% and 30.5% in November and December of 2023. The annual growth rate of retail sales of apparel and online retail sales of wearing goods accelerated by 2.6 and 1.2 percentage points respectively compared with the first three quarters last year.

Figure 1: Sales of Clothing in the Chinese Market in 2023 (Above Designated Size)

Source: National Bureau of Statistics

03 Export

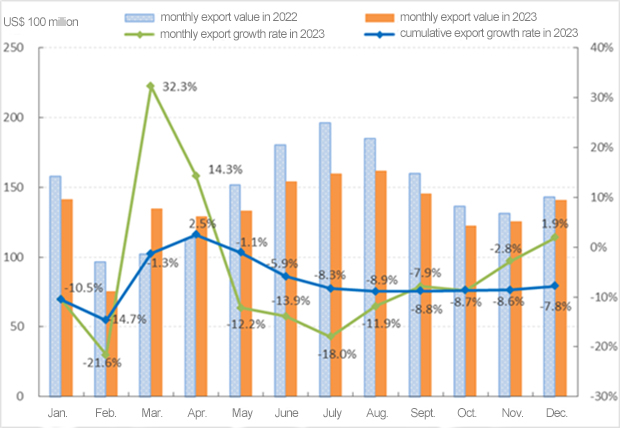

In 2023, due to reduced international market demand and de-risking policies, China's apparel exports continued to slow down in the fourth quarter of last year. The downward pressure on exports increased, leading to a significant decrease in the scale of exports.

According to the Customs Newsletters, China’s apparel and accessories exports totaled US$ 159.14 billion, down 7.8% year-on-year, 11 percentage points slower than the same period of 2022.

Figure 2: Exports of China’s Apparel and Accessories in 2023

Source: China Customs

* all growth rate are in year-on-year terms

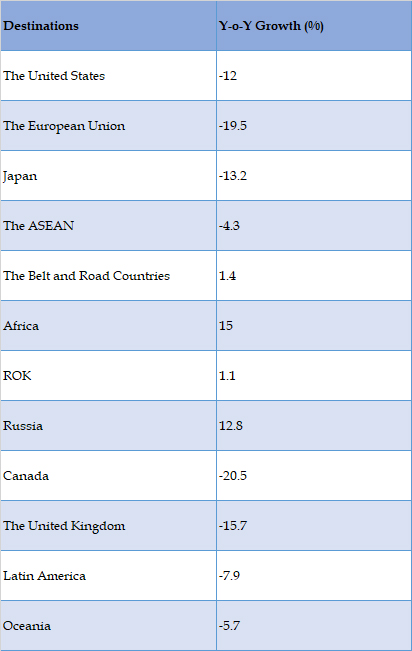

From the main markets' perspective, China’s apparel exports to the United States, the European Union, and Japan kept decreasing, while exports to ASEAN initially rose and then fell. On the other hand, exports to Africa and countries along the Belt and Road showed growth despite the overall trend.

Table 1: China’s Apparel Exports by Destinations in 2023

Source: China Customs

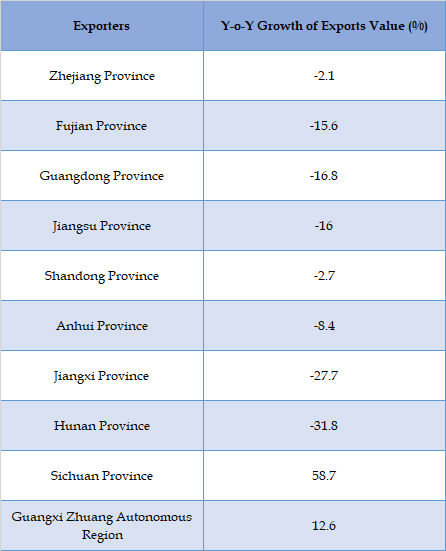

The eastern region of China still holds the dominant position in China’s apparel exports, while the central and western regions continue to see a small increase, particularly in Sichuan, Xinjiang, Guangxi, and other western provinces. This indicates that the shift of the garment industry to the West China is gaining pace.

Table 2: Apparel Exports Performance of China’s Major Exporters in 2023

Source: China Customs

04 Investment

According to the National Bureau of Statistics, the investment in fixed assets in China’s garment industry decreased by 2.2% compared to 2022. The digital transformation and upgrade have accelerated. This involves the development and application of intelligent equipment, intelligent factory construction, supply chain optimization, brand marketing, channel expansion, warehousing, logistics, and various other areas.

Figure 3: Fixed-asset Investment in China’s Textile Industry in 2023

Source: National Bureau of Statistics

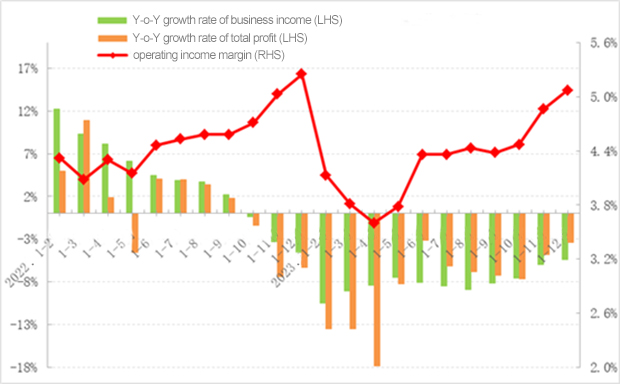

05 Benefit

According to the National Bureau of Statistics, the main business income of apparel enterprises above the designated size totaled about CNY 1.21 trillion, with a year-on-year decline of 5.4%; the total profit was CNY 61.38 billion, down by 3.39% year-on-year. The margin rate of operating was 5.07%, 0.11 percentage points higher than 2022. 20.8% of apparel enterprises above the designated size operated in deficit, 2.07 percentage points higher than that of 2022.

The turnover rate of finished products was 10.71 times/year, down 3.64% year-on-year; the turnover of accounts receivable was 6.40 times/year, seeing a year-on-year decline of 7.65%; and the total asset turnover was 1.11 times/year, down 5.00% year-on-year.

Figure 4: Main Economic Indicators of China’s Apparel Industry in 2023

Source: National Bureau of Statistics

06 Future Outlook

From an international market perspective, apparel exports encounter both favorable and unfavorable factors. The export pressure may not ease in the short term, but there is an expected increase in inventory demand in developed countries, faster growth in emerging markets, and rapid development of new methods like cross-border e-commerce. These developments are expected to result in a stable trend in China’s apparel exports by 2024, as prices improve, and the market structure continues to optimize. The negative factors that are hard to ease in the short term are as follows.

Firstly, trade protectionism and geopolitical risk factors lead to an increase in uncertainty in the international environment. Coupled with the spillover effects of the Ukraine crisis, and the Israeli-Palestinian conflict, as well as the unfolding political elections in the world’s major economies, the international environment will continue to be in a period of turbulent change.

Secondly, the lagged effects of tightening monetary policy will continue to appear. Although Europe and the United States have reached the end of the interest rate hiking cycle, inflation and interest rates continue to remain historically high, which limits the actual purchasing power and consumer confidence of the residents.

Thirdly, the garment industry in Southeast Asia and South Asia countries has gradually recovered. Coupled with the shift in international procurement strategy away from China, this increase in global supply chain competition has put pressure on China's clothing exports. The probability of the RMB appreciating against the U.S. dollar is also worth considering, which may have a certain impact on China's clothing exports.

From the point of view of the domestic market, China’s economic stabilization and good development for the recovery of consumption create good conditions and foundations. It is expected that China's domestic apparel market will continue to recover this year. Several positive factors will continue to support the improvement of the domestic apparel market.

Firstly, the policy on promoting consumption has been effective. Additionally, the employment situation is generally stable, and residents’ income is maintaining growth. This will increase the ability and willingness to consume.

Secondly, as new urbanization and rural revitalization strategies are put into action, e-commerce platforms and brand companies are quickly expanding into second-tier markets. Thirdly, the rise of new consumer groups such as Generation Z, the new middle class, older individuals, and young people from small towns, along with the emergence of new consumer trends such as sportswear, Chinese fashion trends, and sustainability, will continue to boost market vitality and drive the development of new forms and scenes.

Source: CHINA TEXTILE LEADER Express

Authority in Charge: China National Textile and Apparel Council (CNTAC)

Sponsor: China Textile Information Center (CTIC)

ISSN 1003-3025 CN11-1714/TS

© 2026 China Textile Leader, all rights reserved.

Powered by SeekRay