2026/6/24

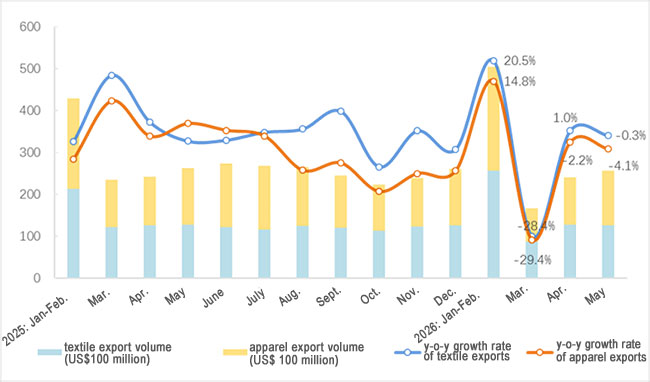

In May, easing China-U.S. trade relations spurred a relatively robust month-on-month growth in apparel exports and a 6.4% month-on-month increase in overall textile and apparel exports. Due to a high base last year, textile and apparel exports declined slightly year-on-year in May, while cumulative exports from January to May showed a marginal increase. According to the latest data released by the General Administration of Customs, in U.S. dollar terms, textile and apparel exports in May amounted to US$25.61 billion, down 2.3% year-on-year but up 6.4% month-on-month. Textile exports reached US$12.59 billion, down 0.3% year-on-year and 0.9% month-on-month, while apparel exports stood at US$13.02 billion, down 4.1% year-on-year but up 14.7% month-on-month. From January to May, cumulative textile and apparel exports totaled US$116.72 billion, up 0.1% year-on-year.

In CNY-denominated terms, from January to May, cumulative textile and apparel exports amounted to 812.24 billion yuan, down 3.1% compared to the same period last year (similarly hereinafter). Textile exports reached 413.94 billion yuan, seeing a decline of 1.5%, while apparel exports totaled 398.3 billion yuan, down 4.7%. In May alone, textile and apparel exports stood at 175.79 billion yuan, representing a year-on-year decrease of 7% but a month-on-month increase of 6.9%. Textile exports were 86.43 billion yuan, down 5.1% year-on-year and 0.5% month-on-month, while apparel exports reached 89.36 billion yuan, down 8.7% year-on-year but up 15.1% month-on-month.

Figure 1: China’s Monthly Statistics of Textile and Apparel Exports (US$100 Million)

This year, the international environment has remained complex and volatile, with global supply chain costs under pressure and end-consumer demand recovering slowly. In the face of external challenges, China’s textile industry has demonstrated resilience in foreign trade: exports to major developed markets such as the United States, the European Union, and the United Kingdom have continued to grow. Exports to countries including Bangladesh, Russia, Australia, India, Brazil, Nigeria, and the RCEP region have outperformed global export growth, with emerging markets becoming a key pillar supporting foreign trade stability. However, amid regional tensions that are driving up energy costs, imports of Chinese textiles and apparel by markets such as ASEAN, Japan, and South Korea have declined. Since May, China-U.S. economic and trade consultations have made phased progress, with marginal reductions in bilateral tariffs, providing some buffer for textile and apparel exports. At the same time, on June 2, the Office of the U.S. Trade Representative (USTR) issued a Section 301 investigation determination, finding that 60 economies failed to implement and effectively enforce measures prohibiting imports of products produced with forced labor, and proposing an additional 12.5% tariff on China (including the Hong Kong region). Further investigations related to the so-called “overcapacity” may follow. Amid overlapping measures, China-U.S. trade still faces potential risks of tariff escalation. Chinese textile foreign trade enterprises need to closely monitor international market dynamics, strengthen risk assessment, and flexibly adjust market strategies. They should also actively expand the domestic market, enhance product innovation and brand development, and comprehensively improve risk resistance and international competitiveness.

Source: CHINA TEXTILE LEADER Express

Authority in Charge: China National Textile and Apparel Council (CNTAC)

Sponsor: China Textile Information Center (CTIC)

ISSN 1003-3025 CN11-1714/TS

© 2026 China Textile Leader, all rights reserved.

Powered by SeekRay