2022/2/21

From January to October, the economic operation of China’s printing and dyeing industry recovered continually. And the main economic indicators also improved. In October, the output of printed and dyed cloth remained at a high level; the export of major products picked up; the quality and efficiency of enterprise operations continued to improve. However, it should also be noted that the growth rate of the main economic indicators of the industry from January to October has declined compared with the first half of 2021 and the third quarter.

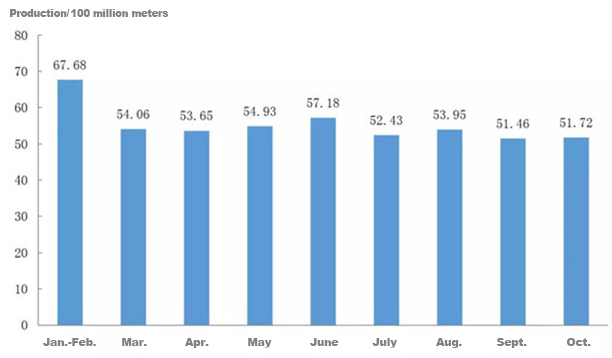

I. Production

According to the National Bureau of Statistics, from January to October, the output of printed and dyed fabrics of enterprises above designated size in the printing and dyeing industry reached over 49.47 billion meters, seeing a year-on-year increase of 17.95%. And the two-year average growth was 5.83%. Since the beginning of 2021, despite the partial spread of the domestic epidemic, the poor connection between supply and demand, and the introduction of power and production restrictions in some domestic provinces, the production of the printing and dyeing industry has maintained a good growth trend. From January to October, the output of printed and dyed cloth of enterprises above designated size has achieved double-digit growth (12%) compared with the same period in 2019. The monthly output in the first 10 months of 2021 has remained at a high level of more than 5 billion meters.

Figure: Monthly Output of Printed and Dyed Fabrics by Enterprises Above Designated Size in January-October 2021

II. Exports

According to the statistics released by China General Customs, from January to November, the export volume of eight major categories of printed and dyed products totaled more than 22.91 billion meters, up 25.03% year-on-year. The two-year average growth reached 1.88%. While the export value was US$ 22.83 billion, seeing a year-on-year rise of 29.75%. The two-year average growth reached 0.76%. And the average export unit price was US$ 1.00/meter, declining by 0.93% year-on-year. Although the export volume and export value have shown a downward trend as a whole, the average growth rate in the two years has achieved a slight increase, indicating that market demand is gradually picking up.

III. Operation Quality

According to data from the National Bureau of Statistics, from January to October, the share of three overheads in turnover of printing and dyeing enterprises above designated size was 6.77%, 0.15 percentage point lower than the same period of 2020. The turnover rate of finished products was 17.95 times / year, up 7.13% year-on-year. The turnover of account receivable was 8.24 times / year, seeing year-on-year rises of 9.43%; and the total asset turnover was 1.01 times / year, up 10.61% year-on-year.

Compared with the same period in 2019, the share of three overheads in turnover increased by 0.02 percentage points, while the turnover rate of finished products and the total asset turnover were reduced by 13.90% and 6.51%, respectively. And the turnover of account receivable grew by 2.44%.

IV. Operation Efficiency

According to the National Bureau of Statistics, from January to September, the main business income of the printing and dyeing enterprises above designated size reached CNY 233.72 billion, up 18.32% year-on-year. The two-year average growth reached 1.58%. Their total profits reached CNY 10.37 billion, with year-on-year growth of 21.06%. The two-year average growth was -3.51%. The profit margin reached 4.75%, up 0.14 percentage points. The ratio of profits to cost was 4.44%, 0.10 percentage point higher than in 2020. 25.37% of printing and dyeing enterprises operated in deficit, declined 8.09 percentage points year-on-year; the loss value of these enterprises fell by 16.70% year-on-year. The completed export delivery value reached CNY 31.32 billion, up by 11.77% year-on-year. The two-year average growth was -4.88%.

From January to October 2021, in the face of the complex and changeable domestic and foreign environment, China’s printing and dyeing industry maintained a recovery trend. Major economic indicators recovered continually; and the economy was operating generally stable. However, there are still many factors of instability and uncertainty. For example, the recovery of domestic and foreign consumer demand has weakened; the profitability of enterprises was affected by the pressure of increasing costs; the variant of the Covid-19 pandemics let lots of countries lockdown again, which wreaked havoc on the supply chain of the textile industry. On the whole, the overall recovery of the printing and dyeing industry is still under great pressure, and the foundation for the industry to maintain a stable recovery still needs to be further consolidated.

Authority in Charge: China National Textile and Apparel Council (CNTAC)

Sponsor: China Textile Information Center (CTIC)

ISSN 1003-3025 CN11-1714/TS

© 2026 China Textile Leader, all rights reserved.

Powered by SeekRay