2021/1/13

In January-September 2020, after the serious hit by the Sino-US trade conflict and the Covid-19 pandemic, China’s economy turned a positive growth, and the economic operation recovered steadily. During this period, the overall operation of China’s Textile Machinery Industry performed better than that of H1. However, it still faced great pressure due to the pandemic.

I. Economic operation

1. Industry scale

In January-September period, the textile machinery industry earned CNY 47.70 billion of prime business income, down 16.04% year-on-year, declining 10.25 percentage points compared with same period of last year; it had more than CNY 99.88 billion of total assets, up 8.59% year-on-year, 0.98 percentage points lower than that of H1, 2020.

2. Structure of costs and expenses

In the first nine months of 2020, the share of three overheads in turnover was 11.08%, up 0.43 percentage points year-on-year. The costs and expenses of the textile machinery totaled about CNY 43.78 billion, declined by 15.7% year-on-year, in which, prime operating costs stood at about CNY 38.93 billion, down 16.14% year-on-year, covering 88.92% of the total; sales expenses amounted to over CNY 1.56 billion, down 18.95%, accounting for 3.58% of the total; management expenses stood at CNY 2.85 billion, down 10.84%, accounting for 6.53% of the total; financial expenses totaled CNY 427 million, up 7.74%, accounting for 0.98% of the total.

3. Profit

In January-September, the textile machinery industry earned over CNY 2.98 billion of profits, declined by 26.48% year-on-year; 28.01% of enterprises operated in red, and their deficit totaled CNY 524 million, surged by 59.4% year-on-year. In January-September, the profit margin of the main business of the textile machinery industry was 6.26%, seeing a year-on-year decline of 0.33 percentage points.

II. Import and Export

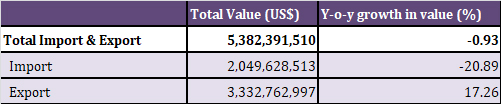

According to the General Administration of the Customs, China’s import and export of textile machinery totaled US$ 5.38 billion in January-September period, down 0.93% year-on-year. The export of textile machinery totaled more than US$ 3.33 billion, up 17.26% year-on-year, while the import stood at US$ 2.05 billion, decreased by 20.89%.

Table 1: Import and Export of Textile Machinery in January- September 2020

1. Import

In January- September period, China imported US$ 2.05 billion worth of textile machinery from 68 countries and regions, down 20.89% year-on-year.

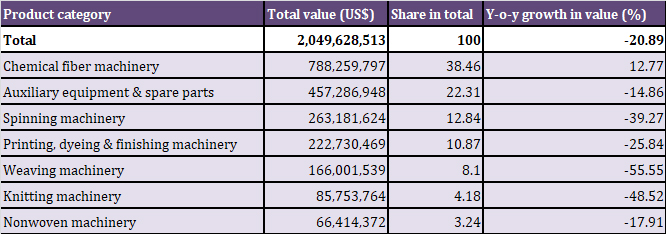

By product category, chemical fiber machinery ranked the first, with import amounting to US$ 788 million, up 12.77% year-on-year, accounting for 38.46% of the total. Except for chemical fiber machinery, the other six categories among seven major product categories saw decline in different degrees.

Table 2: Import of Textile Machinery by Product Category in the First Three Quarters of 2020

Table 3: Import of Major Categories of Textile Machinery by Supplier in January- September 2020

Unit: US$

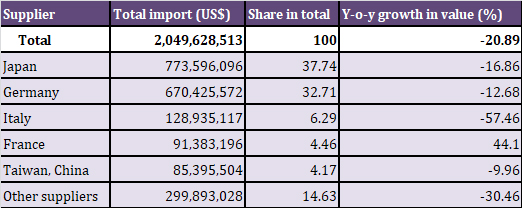

In January-September, the top five suppliers of China’s imported textile machinery are Japan, Germany, Italy, France and Taiwan, China, with a trade volume of US$ 1.75 billion, decreased by 18.98% year-on-year, accounting for 85.37% of the total import.

Table 4: Import of Textile Machinery from Top Suppliers in the First Three Quarters of 2020

2. Export

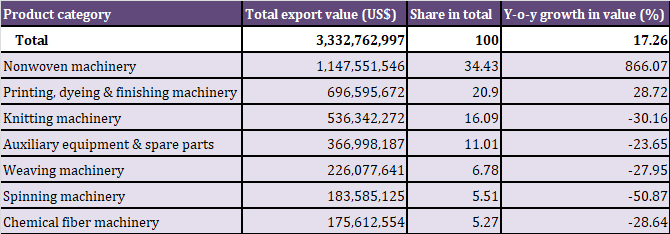

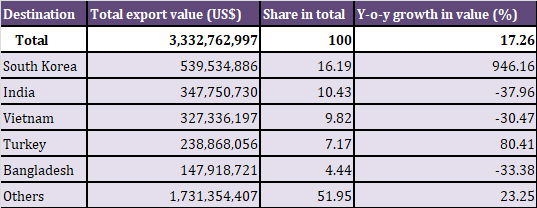

In the first three quarters of 2020, China exported over US$ 3.33 billion worth of textile machinery, up 17.26% year-on-year. Driven by the export of anti-pandemic related machinery, the exports of textile machinery performed better than last year, turning to positive growth.

Table 5: Export of Textile Machinery by Product Category in the First Three Quarters of 2020

In January-September, China exported textile machinery and equipment to 179 countries and regions. The top five destinations are South Korea, India, Vietnam, Turkey, and Bangladesh.

Table 6: Main Destinations of China’s Textile Machinery Export in the First Three Quarters of 2020

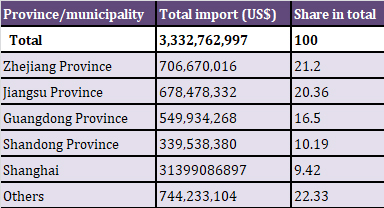

Table 7: Top Five Textile Machinery Exporters in the First Three Quarters of 2020

III. Each sub-industry situation

Table 8: Sales Data of Textile Machinery by Major Chinese Textile Machinery Manufacturers in the First Three Quarters of 2020

1. Spinning machinery

Affected by the Covid-19 pandemic, the overall demand for spinning machinery at home and abroad is sluggish. The continual pandemic has wreaked havoc on the foreign trade and personnel flow. The recovery of the export market still takes a long time. Among imported equipment, only the demand for air-jet vortex spinning equipment is still growing, indicating the hot domestic demand for air-jet vortex spinning. With the stabilized domestic epidemic situation, the potential of domestic demand in China has been continuously released. Coupled with the transfer of some foreign textile orders to China, textile enterprises have gradually recovered after July.

2. Weaving machinery

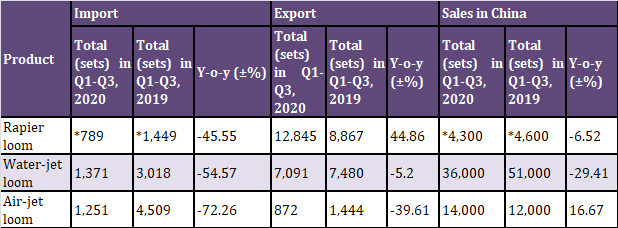

In the first three quarters of 2020, the sales of weaving machinery experienced a sharp decline in the first quarter, and stabilized in the second quarter. The sales of rapier looms and air-jet looms in the third quarter showed a month-on-month growth for the first time this year. Water-jet looms were affected by the huge market stock, its sales in the third quarter were basically the same month-on-month. It is expected that in the fourth quarter of 2020, the annual sales of rapier looms are expected to continue to increase due to the return of textile orders and changes in fabric specifications. The decline in sales of filament fabrics and home textiles will continue to narrow, and the sales of water-jet weaving machinery are expected to pick up gradually. Meanwhile, weaving machinery companies still pay attention to corporate cash flow management, capacity expansion control, and focus on the effect of the pandemic on the domestic consumer market and the international market.

Table 9: Foreign Trade and Sales of Shuttle-less Loom (sets) in the First Three Quarters of 2020

*high-speed rapier loom

3. Knitting machinery

In the first three quarters of 2020, with the recovery of the domestic economy, among the three types of knitting machinery, the circular knitting machine and warp knitting machine industries have gradually improved, but the flat knitting machine industry still faces greater downward pressure. The operation of the flat knitting machine industry in the first three quarters was still severe, and the production and sales dropped significantly. On the one hand, the impact of the Covid-19 pandemic has affected downstream market orders; on the other hand, the number of new machines in the past few years has led to insufficient upgrading of the old equipment in China.

4. Printing, dyeing & finishing machinery

The outbreak of the Covid-19 pandemic has wreaked havoc on textile machinery manufacturers and the global textile and apparel industry chain. In the first half of 2020, the cancellation or postponement of corporate orders is common. With the gradual stabilization of domestic epidemic prevention and control, normal operations have gradually resumed from mid-to-late April, and the market has gradually recovered. According to the association’s statistics, from January to September 2020, the domestic market for major pre-processing equipment was in good condition in the third quarter. In addition, as digital printing equipment is relatively flexible and can better meet the needs of small batches and multi-batch orders in the market during the pandemic, its market situation in the first three quarters is better than that of conventional printing equipment. Driven by the home textile industry, the wide-width digital printing equipment used in home textiles increased slightly compared with the same period last year. On the whole, the market in the third quarter was much better than in the second quarter.

5. Chemical Fiber Machinery

In the first three quarters of 2020, the new production capacity of chemical fiber spinning machines increased slightly, seeing a year-on-year increase of 15.78%. And the new production capacity of viscose equipment improved year-on-year. In recent years, the main development direction of equipment is energy saving, consumption reduction and environmental protection, and the demand for differentiated fiber products and equipment will continue to rise.

6. Nonwovens Machinery

In general, the situation of nonwovens machinery enterprises in the first three quarters is relatively optimistic. However, with the delivery of contract orders and the over-saturation of the meltblown nonwovens market, the high demand for meltblown nonwovens equipment this year has gradually cooled down. The quality assurance issues after the delivery of the production lines are also worthy of attention. At present, the pandemic in some overseas countries and regions is still severe. Nonwovens equipment manufacturers in Europe and the United States have continuously increased the production capacity of nonwovens through continuous innovation of technologies and rapid after-sales services, so as to fill the demand gaps of personal protective equipment (PPE) such as surgical masks, protective apparel. In contrast, China’s nonwovens equipment is still competitive in Latin America, Africa, Central Asia, South Asia, Southeast Asia, etc.

IV. Industry outlook

The economic operation of China’s textile machinery industry in the fourth quarter and 2021 is still facing several risks and pressures. The Covid-19 pandemic delivered a blow to the global economy. According to the IMF prediction, the global economy will shrink by 4.4% in 2020. The world today faces profound changes of a kind unseen in a century. The international environment is becoming increasingly complex and volatile. The whole industry will face a series of problems, including pressure on global supply chain cooperation, sharp decline in trade and investment, massive loss of employment opportunities, and geopolitical conflicts. Although the domestic and foreign market demand has picked up in the textile industry, it has not yet returned to a normal level, and the investment confidence of enterprises still needs to be restored. In addition, according to the latest survey report issued by the International Textile Manufacturers Federation (ITMF) in September this year, the turnover of major textile companies in the world is expected to drop by an average of 16% in 2020 due to the pandemic. It is expected that it will take several years to fully compensate for the losses. In this context, the market adjustment of the textile machinery industry is still continuing, and the pressure on enterprise production and operation has not yet eased.

Authority in Charge: China National Textile and Apparel Council (CNTAC)

Sponsor: China Textile Information Center (CTIC)

ISSN 1003-3025 CN11-1714/TS

© 2026 China Textile Leader, all rights reserved.

Powered by SeekRay