2026/3/20

In 2025, faced with complex and challenging external conditions such as persistent weak international demand and volatile US tariff policies, along with practical issues like sluggish domestic consumption growth and subdued market expectations, China’s garment industry continued to deepen its transformation and upgrade. It steadily promoted development, resilience, and innovative vitality. Supported by a stable macroeconomic environment with consistent progress and the combined effects of various existing and new policies, the industry’s economic performance demonstrated a trend of “basic stability and steady progress under pressure”. Looking ahead to 2026, many uncertainties still weigh on China’s garment industry. The sector must follow the development focus of “technology, fashion, green, and health”, promote deep structural adjustments and upgrades in the industry, accelerate the cultivation of new high-quality productive forces, and create a new scenario for high-quality industrial development.

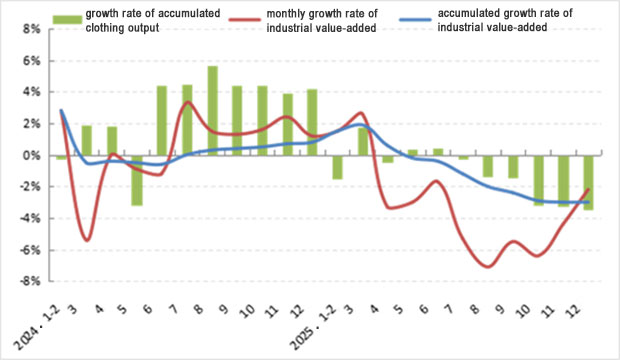

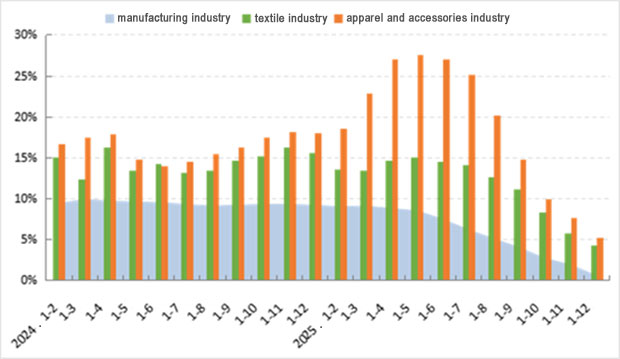

A. Slight Contraction in Output Scale

In 2025, the production scale of China’s garment industry contracted slightly, with industrial value-added continuing to contract and the rate of decline gradually deepening. This is not only the result of the combined effects of complex and changeable international situations and generally weak terminal market demand, but is also closely related to the industry’s transformation and upgrading. The enhancement of flexible manufacturing capabilities has accelerated the shift in garment production models towards leaner, more effective production. According to data from the National Bureau of Statistics, in 2025, the industrial value-added of enterprises above the designated size in the garment industry decreased by 3.0% year-on-year, a narrowing of the decline by 3.8 percentage points compared to the same period in 2024. The garment output of enterprises above the designated size decreased by 3.44% year-on-year, with the growth rate falling by 7.66 percentage points from the same period in 2024.

Figure 1: Growth Rate of China’s Apparel Industry Output in 2025

Source: National Bureau of Statistics

In terms of output by major garment categories, the decline in woven garment output was higher than that of knitted garments. From January to December, woven garment output decreased by 5.03% year-on-year, with the decline deepening by 3.04 percentage points compared to the same period in 2024. Among them, the output of down apparel, suit sets, and shirts decreased by 0.77%, 17.54%, and 8.93% year-on-year, respectively. Knitted garment output declined by 2.71% year-on-year, with the growth rate falling by 10.09 percentage points compared to the same period in 2024.

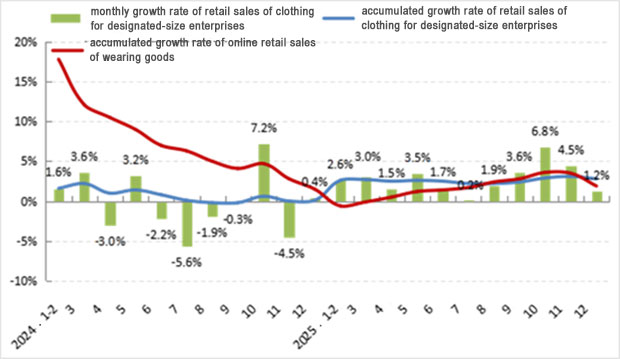

B. Moderate Growth in the Domestic Sales Market

In 2025, supported by positive factors such as the solid advancement of national special actions to boost consumption and sustained stimulation of market vitality through new consumption models, demand for residents’ apparel gradually emerged, and the domestic garment sales market maintained moderate growth. According to data from the National Bureau of Statistics, in 2025, retail sales of apparel by enterprises above designated size in China reached 1.1 trillion yuan, up 2.8% year-on-year, accelerating by 2.7 percentage points from the same period in 2024. Online retail sales of wearing goods increased by 1.9% year-on-year, with the growth rate accelerating by 0.4 percentage points compared to 2024.

Figure 2: Sales Performance of Apparel in China’s Domestic Market in 2025

Source: National Bureau of Statistics

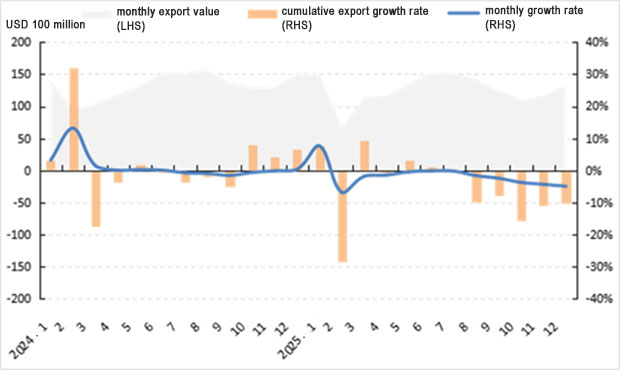

C. Increased Downward Pressure on Exports

In 2025, affected by multiple complex factors, including weak recovery in international market demand, disruptions from volatile US tariff policies, and accelerated restructuring of the global garment supply chain, pressure on China’s garment exports intensified, and export volumes declined significantly. According to China Customs data, in 2025, China’s cumulative exports of apparel and accessories amounted to US$151.18 billion, down 5.0% year-on-year, with the growth rate falling by 5.3 percentage points compared with the same period in 2024. In terms of the volume-price relationship, garment exports continued the trend of increased volume but decreased prices. The export volume was 35.65 billion pieces, up 4.3% year-on-year, while the average export unit price was US$3.5/piece, down 8.6% year-on-year.

Figure 3: China’s Apparel and Accessories Exports in 2025

Source: National Bureau of Statistics

In terms of product categories, most sub-categories showed a trend of increased volume but decreased prices, with woven garments experiencing a particularly significant decline in export prices. In 2025, the export value of knitted garments was US$68.15 billion, down 4.3% year-on-year, while export volume increased by 3.9% and the average export unit price fell by 7.9%. The export value of woven garments was US$56.78 billion, down 5.2% year-on-year, with export volume rising by 5.0% and the average export unit price dropping by 9.7%. Among specific sub-categories, the export value of casual suits grew by 13.1% year-on-year, and sweater exports remained flat compared to the same period in 2024, while exports of other major garment categories declined. The export values of tops, trousers, and T-shirts decreased by 7.3%, 0.5%, and 8.9% year-on-year, respectively. In contrast, down jackets saw a decrease in volume but an increase in price, with export volume falling by 22.2% and the average export unit price rising by 7.6% year-on-year.

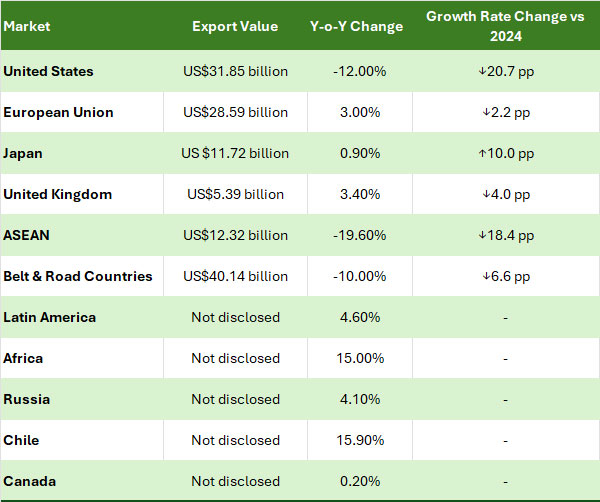

From the perspective of major markets, impacted by factors such as U.S. tariff policies and inspections on re-export trade, China’s garment exports to the United States have fallen significantly, while the decline in exports to ASEAN and countries along the “Belt and Road” has worsened. In contrast, exports to markets such as the EU, Japan, and the UK have remained steady, while shipments to emerging markets such as Latin America and Africa have continued to grow rapidly. As a result, the trend of diversification in China’s garment export markets has become more apparent.

Table: China’s Apparel Export Data by Major Markets (Jan.-Dec. 2025)

D. Significant Slowdown in Investment Growth

In 2025, the government promoted increased private-sector involvement in major national projects and initiatives, including those aligned with key national strategies, enhancing security capacity in critical areas, and the large-scale renewal of equipment and trade-ins of consumer goods. China’s garment industry actively boosted investment in areas like technological upgrades, brand innovation, and channel development. Overall fixed-asset investment in the industry maintained relatively rapid growth, although the growth rate slowed considerably. According to data from the National Bureau of Statistics, in 2025, the total fixed-asset investment in China’s garment industry rose by 5.2% year-on-year. The growth rate dropped by 12.8 percentage points compared to the same period in 2024, but still remained 0.9 and 4.6 percentage points higher than the overall levels for the textile industry and the manufacturing sector, respectively.

Figure 4: Growth Rate of Fixed-asset Investment in China’s Apparel Industry in 2025

Source: National Bureau of Statistics

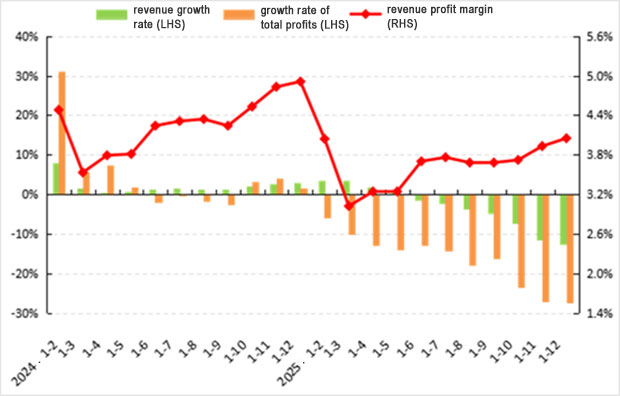

E. Severe Pressure on Operational Quality and Efficiency

In 2025, the interplay of weak terminal demand, intensified competitive pressures, and high operating costs severely strained the operational quality and efficiency of China’s garment industry. The decline in operating income and total profits continued to deepen, and corporate profitability dropped significantly. According to data from the National Bureau of Statistics, in 2025, there were 13,745 enterprises above the designated size (with annual main business income of 20 million yuan or more) in China’s garment industry, with operating income of 1.11 trillion yuan, a year-on-year decrease of 12.67%. Their total profits were 45.06 billion yuan, down by 27.34% year-on-year. The operating profit margin was 4.05%, 0.82 percentage points lower than in the same period in 2024. (Figure 5)

Figure 5: Key Performance Indicators of China’s Apparel Industry in 2025

Source: National Bureau of Statistics

The industry’s losses have widened, and operational efficiency has dropped. From January to December, the loss-making ratio for enterprises above the designated size in the garment industry reached 22.61%, up 3.48 percentage points from the same period in 2024. The ratio of the three major expenses was 10.35%, an increase of 0.73 percentage points year-on-year. Costs amounted to 84.52 yuan per 100 yuan of operating revenue, up 0.08 yuan from the same period in 2024. The turnover rates for finished goods, accounts receivable, and total assets were 9.69, 5.40, and 1.05 times per year, respectively, reflecting year-on-year decreases of 9.14%, 16.34%, and 12.27%. This slowdown in turnover indicates increasing operational pressure across the industry.

Source: CHINA TEXTILE LEADER Express

Authority in Charge: China National Textile and Apparel Council (CNTAC)

Sponsor: China Textile Information Center (CTIC)

ISSN 1003-3025 CN11-1714/TS

© 2026 China Textile Leader, all rights reserved.

Powered by SeekRay