2026/3/20

In 2025, China’s knitting industry faced a complex and volatile external environment. Multiple challenges intertwined and overlapped, including the impact of U.S. tariffs, weak market demand, intensified geopolitical conflicts, and deep adjustments in the global supply chain. Meanwhile, the foundation for domestic economic recovery still needs strengthening. Relying on its comprehensive industrial chain advantages and strong market adaptability, the industry demonstrated structural resilience amidst overall pressure. Its operation was marked by “optimized production structure, robust domestic demand support, shifting export patterns, and divergent performance under profit pressures.” Although core indicators like revenue and profits declined year-over-year, exports of knitted fabrics continued to grow; the domestic sales market experienced a moderate recovery; product structures shifted toward high-end and functional categories; and progress was made in market diversification. At the same time, the industry faces significant challenges, including cost pressures, market competition, and global supply chain restructuring. There is an urgent need to promote high-quality development through measures such as technological innovation, improvements in quality and efficiency, and layout optimization.

A. Revenue Declined, While Knitted Garment Output Remained High

Revenue decreased year-on-year. According to statistics from the National Bureau of Statistics, in 2025, the operating revenue of enterprises above the designated size in the knitting industry fell by 12.15% year-on-year (Figure 1). Breaking it down by category: the operating revenue of knitted fabric enterprises above the designated size dropped by 14.61%, while that of knitted garment enterprises decreased by 10.77%. Throughout the year, the industry’s revenue growth rate turned negative in the second quarter and accelerated its decline, showing a downward trend period by period. This reflects the continuous impact of insufficient market demand and intensified competition on industry revenue.

Figure 1 Growth Rate of Revenue of Scale-above Knitting Enterprises since 2024

Source: National Bureau of Statistics

Continuous Emergence of Industrial Innovation. Despite operational pressures, the industry has witnessed numerous highlights. The lace market has warmed up, the pet apparel sector is rising, and the sports market continues to grow. The surge in mass-participation sports events, such as “Su Chao” (Jiangsu Super League), has driven sales of sportswear and related products like artificial turf. Knitted products are extending into the home bedding category. Furthermore, Xiaomi’s entry into the automotive sector has spurred the use of flat-knitting machine products in automotive interiors. Innovations such as electronic skin apparel, dexterous robotic hands, and smart apparel demonstrate the knitting industry’s vitality and its characteristic ability to “knit everything”.

Market Share of Knitted Garments Continues to Consolidate. In 2025, the garment output of enterprises above the designated size in China’s textile and garment industry totaled 20.25 billion pieces, down 3.44% year-on-year. Among these, the output of knitted garments was 14.02 billion pieces, down 2.71% year on year (Figure 2). This decline rate is lower than the overall level of total garment output, indicating relatively robust market demand for knitted garments. In 2025, the proportion of knitted garment output in total garment output reached 69.24%, a slight increase from 68.35% in 2024, further consolidating the industry’s structural advantage.

Figure 2 Output and Growth Rate of Apparel in China’s Textile and Apparel Industry (Enterprises Above Designated Size) since 2024

Source: National Bureau of Statistics

B. Operational Quality and Efficiency Under Pressure; Industry Structure Shows Polarization

Total Profits Declined Sharply. In 2025, the total profits of large-scale knitting enterprises fell by 26.18% year-on-year, a larger decline than that in operating revenue, indicating significantly increased pressure on industry profitability. Breaking it down by category: total profits for knitted fabrics dropped by 18.42%, while total profits for knitted garments plummeted by 30.18%, with the latter experiencing a more significant downturn. The primary causes include weak consumer demand driven by domestic economic conditions and international market fluctuations, intensified market competition, rising cost factors, severe product homogenization, fierce price wars, and the appreciation of the Renminbi.

Profit Margins Continued to Fall. In 2025, the operating profit margin for the knitting industry was 3.77%, a decrease of 0.84 percentage points from 4.61% in the same period of 2024. Specifically, the operating profit margin for knitted fabrics was 4.07%, down 0.44 percentage points from 4.51% in 2024; the operating profit margin for knitted garments was 3.61%, down 1.05 percentage points from 4.66% in 2024.

Loss-Making Scope Widens. In 2025, the percentage of loss-making enterprises in the knitting industry reached 19.56%. It increased by 1.32 percentage points compared to 18.24% in the same period of 2024. Among these, the loss-making ratio for knitted fabrics was 16.84% (up 1.6 percentage points), and for knitted garments, it was 21.14% (up 1.18 percentage points). Additionally, the proportion of the three major expense categories (selling, administrative, and financial) increased.

Table 1: Main Operating Indicators of Enterprises Above Designated Size in the Knitting Industry in 2025

Source: National Bureau of Statistics

Leading Enterprises Achieve Counter-Cyclical Growth. Despite overall operational pressures in the industry, leading companies such as Shenzhou International Group and Zhejiang Jasan Holding Group Co., Ltd. have demonstrated strong competitive advantages in the market. By relying on lean management, robust design and R&D capabilities, forward-looking international capacity layout, channel innovation, and supply chain integration, these flagship enterprises have maintained a high-growth trajectory even amid adverse conditions. Their growth rates in operating revenue and total profits, as well as their profit margins, far exceed the industry average, providing a roadmap for the industry’s transformation and upgrading.

C. Slight Decline in Exports, Significant Achievements in Market Diversification

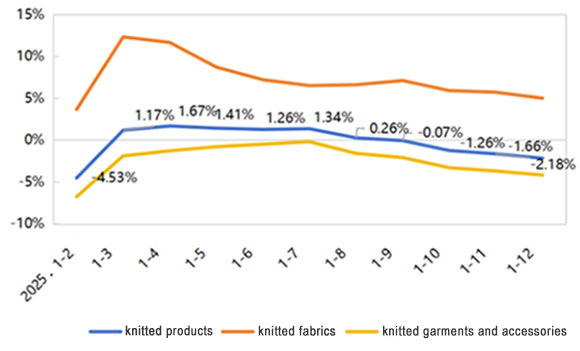

According to data from China Customs, despite adverse factors such as U.S. tariff policies, China’s knitted product exports totaled US$106.65 billion in 2025, down 2.18% year-on-year (Figure 3). This marks a slight decline against a high base, yet exports have remained above the US$100 billion threshold for five consecutive years. Breaking down by category: exports of knitted fabrics reached US$24.95 billion, up 4.99% year-on-year, maintaining steady growth; meanwhile, exports of knitted garments and accessories amounted to US$81.7 billion, down 4.18% year-on-year, serving as the primary factor dragging down the overall export growth rate. Analyzing the trend of cumulative monthly growth rates, export growth for knitted products was generally positive in the first eight months of 2025 but turned negative starting in September. This shift reflects the continuous weakening of international market demand and the profound impact of tariffs on the restructuring of global supply chains.

Figure 3: Cumulative Export Growth Rate of China’s Knitted Products in 2025

Source: China Customs

Deep Adjustment in Export Market Patterns. In 2025, influenced by tariff policies, exports to the United States fell to US$19.54 billion, a year-on-year decrease of 9.41%. Chinese products faced structural compression in the U.S. market share. According to data from the U.S. Department of Commerce, from January to September 2025, China’s share of knitted product imports in the U.S. plummeted from 22.13% in 2024 to 15.18%. In contrast, Vietnam’s market share rose to 20.47%, surpassing China for the first time, indicating a clear trend of orders shifting toward Southeast Asian countries such as Vietnam and Cambodia.

Exports to the European Union reached US$15.992 billion, achieving a counter-trend growth of 3.95%. Data from Eurostat shows that from January to October 2025, China’s share of knitted products in EU import trade rebounded from 29.32% in 2024 to 29.87%, leading the second-ranked Bangladesh by 5.08 percentage points, demonstrating the industry’s export resilience. Exports to Japan totaled US$6.72 billion, representing a 3.14% increase. However, according to Japan Customs data, from January to November 2025, China’s share of knitted products in Japan’s import trade slightly declined from 52.81% in 2024 to 51.25%, continuing a downward trend.

Exports to the ten ASEAN nations amounted to US$17.86 billion, down by 4.56% year-on-year. Conversely, exports of knitted fabrics to this region grew by 6.33% year-on-year. This divergence reflects the impact of U.S. tariff policies on finished goods re-export trade and highlights the competitive advantage of Chinese knitted fabrics in the ASEAN market.

Emerging Markets Become New Growth Engines. Facing the profound restructuring of global supply chains triggered by trade protectionism and U.S. tariff policies, the industry has proactively adopted a diversified market strategy. Through optimizing international capacity layout and actively developing emerging markets, the sector has effectively hedged against external risks. Regions along the “Belt and Road” initiative and other emerging markets in Central Asia, the Middle East, Africa, and South America have emerged as new growth points.

In 2025, exports to Chile reached US$1.55 billion, up 17.48% year-on-year, primarily driven by knitted garments. Exports to Egypt totaled US$774 million, surging 31.19%, with knitted fabrics being the main category. Exports to Kenya amounted to US$547 million, up 28.82%, where knitted garments accounted for a significant share. Notably, exports to Argentina hit US$454 million, skyrocketing by 98.87%; within this, knitted garment exports grew by over 179.4%, demonstrating the immense potential of emerging markets. Although the current base remains relatively small, these markets have become a vital emerging force driving export growth and dispersing market risks.

Significant Regional Export Divergence; Xinjiang Emerges as a New Strategic Pivot. Coastal provinces in eastern China, leveraging advantages such as industrial clusters and supply chain support, remain the main force in exports. In 2025, Zhejiang and Shandong Provinces maintained growth, with export values increasing by 5.23% and 2.26% year-on-year, respectively. Jiangsu Province saw a slight decline of 2.29%, remaining overall stable. However, Guangdong and Fujian Provinces faced pressure from export adjustments, with declines of 8.09% and 12.89%, respectively.

Exports from central, western, and border regions showed differentiated trends. Benefiting from recent government policy support, Hubei achieved a 4.87% year-on-year growth, while Guangxi and Jiangxi saw decreases of 6.39% and 3.49%, respectively. Behind this regional divergence lie a combination of factors, including industrial transfer, policy support, and market radiation, which provide direction for optimizing the industry’s regional layout.

Xinjiang has emerged prominently as a new strategic pivot. Although its export value in 2025 decreased by 13.18% year-on-year due to short-term trade fluctuations, its role is critical. Leveraging its location as the core zone of the “Belt and Road”, an increasingly complete textile industry chain, and unique market channels facing Central Asia, Xinjiang has become a key springboard for the industry to explore Eurasian markets and an important hub for capacity transfer, holding immense long-term growth potential.

Export Categories Saw Volume Increases While Prices Drop; Export Structure Climbs Up the Value Chain. In 2025, exports of raised fabrics, warp-knitted fabrics, and knitted shirts grew by 7.46%, 6.49%, and 9.28%, respectively. Notably, the share of knitted shirts in total shirt exports rose to 33.25%, up 4.42 percentage points year-on-year. Conversely, affected by a high base from the previous year, exports of T-shirts and singlets, underwear and loungewear, and sportswear declined by 8.93%, 10.47%, and 11.54%, respectively.

Exports of knitted fabrics maintained a continuous growth trend, with their proportion in total knitted product exports steadily increasing. Technological advancements are driving the export structure upward along the value chain. On the other hand, most major categories experienced a phenomenon of “increased volume but decreased prices”. This reflects that, against the backdrop of diminishing labor cost advantages, low value-added products face particularly fierce international competition. Enterprises must rely on technological innovation to accelerate the development of high value-added, differentiated products featuring premium quality, functionality, and sustainability. The industry needs to transform from an OEM model reliant on low-cost scale advantages to an ODM model and a brand-oriented strategy anchored in technology, design, and rapid-response capabilities.

D. Moderate Recovery in the Domestic Market, Continuous Release of Consumption Potential

Sustained Growth in Domestic Sales Scale. Driven by the dual forces of domestic macroeconomic policies and innovation in consumption scenarios, the domestic market for the knitting industry has demonstrated strong resilience and vitality. In 2025, the cumulative retail sales of apparel, foot & head wear, and textile products by enterprises above a designated size nationwide reached 1.52 trillion yuan, up 3.2% year-on-year. This growth rate was roughly in line with total retail sales of consumer goods. Particularly during the year-end consumption peak season, market activity improved significantly. In November alone, retail sales showed accelerated growth both year-on-year and month-on-month, effectively offsetting the impact of weak external demand and serving as a “ballast stone” for the industry’s stable operations.

Continuous Development of Online Channels and New Consumption Drivers. In 2025, online retail sales of clothing grew by 1.9% year-on-year. Meanwhile, the trend of consumption upgrading is evident, with robust demand in niche sectors such as domestic trendy brands, health and wellness, sports and outdoor activities, functional apparel, and smart wearables. Brand enterprises are constantly exploring and creating new consumption demands through product innovation, cultural empowerment, and scenario-based marketing. These efforts are driving the domestic market to upgrade from homogenized competition towards a direction characterized by differentiation, quality enhancement, and personalization.

Source: CHINA TEXTILE LEADER Express

Authority in Charge: China National Textile and Apparel Council (CNTAC)

Sponsor: China Textile Information Center (CTIC)

ISSN 1003-3025 CN11-1714/TS

© 2026 China Textile Leader, all rights reserved.

Powered by SeekRay