2024/4/16

In 2023, China’s economy resumed its growth, showing a positive trend, and supply and demand steadily improved, providing essential conditions and support for the smooth operation and development of the textile and chemical fiber industry chain. The annual economic performance of China’s chemical fiber industry has shown a positive trend against this backdrop. Firstly, the industry’s production and sales were stable, and the market was relatively steady. Secondly, the exports of chemical fibers continued to grow, reaching a new record high in export volume. Thirdly, the industry’s operating conditions gradually improved month-on-month, especially in the second half of the year. Fourthly, the high-performance fibers and biobased fibers industry continues to develop steadily.

I.Operation Analysis of China’s Chemical Fiber Industry in 2023

A. Production & Sales

In 2023, the growth rate of chemical fiber output increased compared to 2022. For one thing, due to market conditions, part production plan for 2022 was delayed to 2023. For another, the industry’s overall production capacity at the beginning of 2023 is higher than the same period of the previous year. In the first quarter of 2023, the average production capacity of direct-spun polyester filament was about 67% due to the Spring Festival holiday. This figure rose to about 84% in the second quarter and reached about 90% in the third and fourth quarters. Comparing the average production capacity with that of 2022, there has been a 10-percentage points improvement.

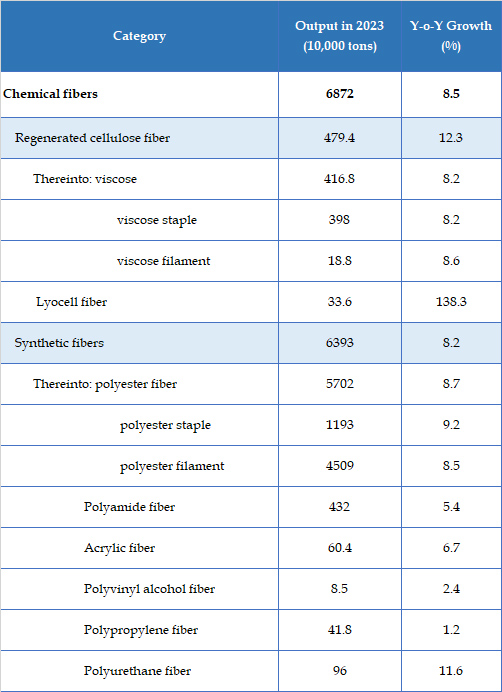

According to the National Bureau of Statistics, the output of chemical fibers in 2023 totaled 68.72 million tons, seeing year-on-year growth of 8.5%.

Table 1: Output of China’s Chemical Fiber in 2023

Note: The statistical caliber of the CCFA was adjusted in 2023. Polyester staple fiber includes all the regenerated polyester staple fiber, while polyester filament does not include post-processing products. Meanwhile, in 2022, the base also made adjustments following the same standard.

Source: China Chemical Fibers Association (CCFA)

B. Domestic & External Demand

Benefiting from recovered social communication, the textile industry showed strong resilience, with a noticeable recovery in domestic textile and apparel retail. Data from the National Bureau of Statistics show that the retail sales of clothing, foot & head wear, and knitted goods above designated size increased by 12.9% year-on-year in 2023, with a sharp growth rate of 19.4 percentage points higher than that of 2022. The growth rate of online retailing made a strong recovery, experiencing a 10.8% year-on-year growth in 2023, which is 7.3 percentage points higher than that in 2022.

Affected by reduced overseas demand and increasing trade risks, China’s textile industry faced growing export pressure in 2023. But the development resilience in the field of foreign trade remained. Exports to countries involved in the “Belt and Road” initiative have shown stronger growth, helping offset a partial decline in textile and apparel exports. In 2023, China’s textile and clothing exports totaled US$ 293.64 billion, showing an 8.1% decrease from the previous year, which was 10.6 percentage points lower than in 2022. Among the major export products, the export value of textiles (incl. textile yarns, fabrics and manufactured products) amounted to US$ 134.5 billion, down by 8.3% year-on-year. And the export of apparel amounted to US$ 159.14 billion, seeing a year-on-year decrease of 7.8%. As for the main export markets, China’s textile and apparel exports to the United States, the European Union, Japan, and other markets have decreased compared to the previous year, while exports to Turkey, Russia, and other countries along the “Belt and Road” route have steadily increased.

Overall, the final demand improved compared to 2022, resulting in a stronger direct downstream demand for chemical fiber than in the same period in 2022. The initial rates for major downstream industries of chemical fiber, including loom and polyester yarn, have been high in recent years. From the perspective of China Textile City’s turnover, it has been slightly better than the same period in 2022, especially after September.

C. Foreign Trade

In recent years, the division of labor in the global textile industry has become more prominent. There is increased trading activity in intermediate products at the beginning of the industrial chain, which reflects the integration of the supply chain.

China’s chemical fiber industry plays a core role in the international textile supply chain. According to China Customs data, the exports of chemical fiber in 2023 totaled 6.5 million tons, indicating a growth of 15.08% compared to the previous year (Table 2). Exports of chemical fiber made up 9.47% of the total, which was a 0.76 percentage point increase from 2022. Among these, the export growth of polyester filament and polyester staple fiber has increased by more than 20% year-on-year. For instance, the monthly average exports of polyester staple fiber have reached 100,000 tons, significantly exceeding the levels of previous years.

From the major export destinations perspective, India, Turkey, Vietnam, Pakistan, Egypt, and Brazil are among the top six. The destination has shifted its focus to emerging textile markets. Thereinto, China exported 702,600 tons of chemical fibers to India, which surged by 45.49% year-on-year, accounting for more than 10% of the total; that to Turkey reached 628,000 tons, seeing an increase of 30.54% year-on-year, accounting for 9.65%; to Vietnam totaled 609,500 tons, up by 12.73% year-on-year, accounting for 9.37% of the total.

Table 2: Foreign Trade of Chemical Fiber Products in 2023

Source: Based on data from Chinese Customs

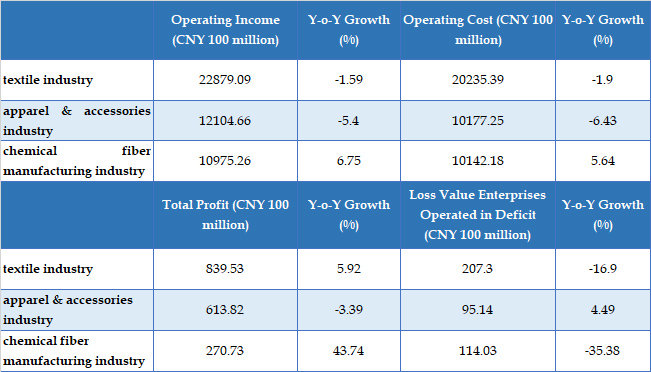

D. Revenue & Benefits

In 2023, the economic indicators for the chemical fiber industry show a positive trend. There is a sharp increase in profits. On one hand, the significant improvement in the industry’s economic performance in the second half of the year is driving this increase; on the other hand, it can also be attributed to the lower base of the fourth quarter of 2022. (See details in Table 3)

In the sub-industry, the polyester, polyamide, acrylic, and spandex sectors contributed approximately 39%, 19%, 1%, and 5% of the total chemical fiber profits. The profits of the polyester industry notably increased.

Table 3: Economic Benefit of Chemical Fiber and Related Industries in 2023

Source: National Bureau of Statistics

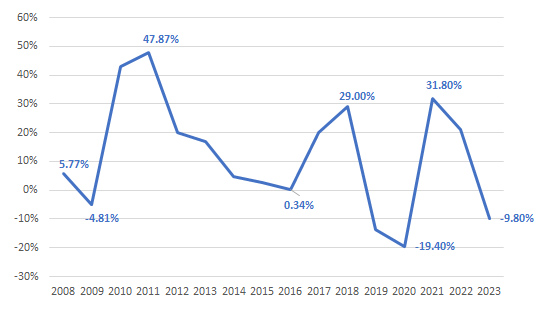

E. Fixed-assets Investment

The National Bureau of Statistics data indicates that the fixed-asset investment in the chemical fiber industry decreased by 9.80% in 2023 compared to the previous year (Figure 2). However, in terms of actual new production capacity, 2023 still witnessed concentrated investment, leading to an inertial growth in the production capacity of the chemical fiber industry. The decrease in fixed asset investment suggests that the current growth phase of the chemical fiber industry is ending, and there will be less pressure on new capacity in the industry in the near future.

Figure: Fixed-Assets Investment Growth of the Chemical Fiber Industry from 2008 to 2023

Source: National Bureau of Statistics

II. Outlook For 2024

The Central Economic Work Conference requires that the country will continue to act on the principle of seeking progress while maintaining stability, promoting stability through progress, and establishing the new before abolishing the old. By implementing policies that support stabilizing growth and employment, the foundation of stability and improvement will continuously be strengthened. The economic performance of China’s chemical fiber industry will continue to improve in this situation.

Since the Spring Festival, there has been a buildup of inventory for all types of chemical fibers. Due to rainy and snowy weather following the holiday, the sales have been delayed. Looking ahead to 2024, China’s textile and clothing consumer demand remains strong in the domestic market. Moreover, the expansion of technical textiles applications and the emergence of new forms of network retailing will continue to generate new consumer demand. With the changes in China’s textile industry’s international division of labor, the foreign trade structure is being adjusted. It is expected that the export share of chemical fiber and its products will continue to show good growth. And the pressure of new production capacity will be eased. However, the release of new capacity accumulated in the past two years still needs to be digested by the market.

Additionally, the uncertainty of crude oil prices will continue to have a significant impact on the chemical fiber economy’s operations. In the current weak global economic growth context, the demand for crude oil will stay under pressure, while the supply side remains relatively abundant. OPEC+ is likely to continue controlling production to sustain oil prices. From a financial perspective, the Fed is likely to reduce interest rates, which will support oil prices. Overall, the global energy market is seeking a balanced adjustment. The geopolitical situation changes, the Federal Reserve interest rate cut process, and the U.S. presidential election may bring substantial fluctuations in international oil prices.

The year 2024 is crucial for achieving the goals and tasks of the “14th Five-Year Plan”. The Central Economic Work Conference has prioritized "building a modernized industrial system through scientific and technological innovation" as the first of the nine key tasks for 2024. The chemical fiber industry will focus on developing new quality productive forces and promoting high-quality development and establishing a high-quality modern industrial system for textile and chemical fibers. Strengthening technological innovation, product innovation, and expand market demand to promote cutting-edge technology, functionality, intelligent wear, biological sources, high-performance fibers, and key equipment. Increase the adoption of digital technology to develop smart factories and create a new industrial framework using the Industrial Internet. By promoting energy-saving, reduced emissions, green energy, recycling, and biodegradability, low-carbon technology guides green consumption and advocates for the dual-carbon strategy.

Source: CHINA TEXTILE LEADER Express

Authority in Charge: China National Textile and Apparel Council (CNTAC)

Sponsor: China Textile Information Center (CTIC)

ISSN 1003-3025 CN11-1714/TS

© 2026 China Textile Leader, all rights reserved.

Powered by SeekRay